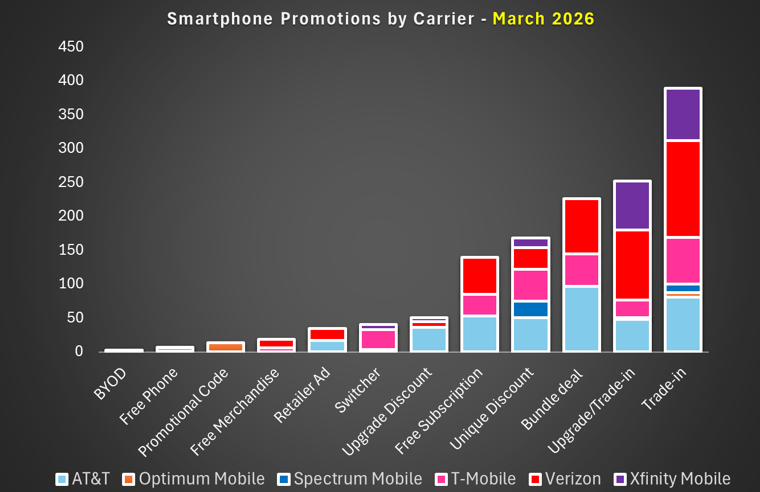

March 2026 reinforces that the US wireless market is in a mature, heavily engineered promotional phase: Handset offers are no longer primarily discounts but mechanisms to control customer behaviour, including upgrade timing, plan selection, multi-line attachment, and churn risk.

Verizon: Premiumization leader with the strongest laddering

Verizon is the most assertive in using handset promotions to force plan migration. Trade-ins and upgrade offers dominate, but value is explicitly gated by unlimited tier, with the richest credits tied to Verizon’s Unlimited Ultimate. New-line offers are broad enough to keep switcher momentum, while existing customers face tighter requirements—confirming Verizon’s intent to monetise its base.

Go deeper with GlobalData

Access deeper industry intelligence

Experience unmatched clarity with a single platform that combines unique data, AI, and human expertise.

AT&T: Most repeatable, retention-weighted value system

AT&T is optimising for predictable growth and controlled acquisition costs, with convergence and digital user experience as retention multipliers. AT&T’s mix (bundles, trade-ins, and free subscriptions) points to a scalable value architecture designed to be run continuously without subsidy spikes. Its Apple iPhone-style offers lean on low monthly pricing + bill credits, extending customer lock-in and smoothing subsidy expense. Its app consolidation and tier simplification strengthen the service layer by improving self-serve retention and cross-sell paths.

T-Mobile: highest cadence, always-on segmentation machine

T-Mobile remains the most active at manufacturing multiple entry points to defend growth, using offers to steer customers upward over time. T-Mobile’s promotions show constant refresh and sharp segmentation: entry-level Essentials plans as the on-ramp, with escalating subsidies tied to T-Mobile Experience More/Beyond. The carrier continues to trade device subsidy for plan margin and multi-line households, sustaining switcher appeal without abandoning premium ARPU goals.

Spectrum Mobile: subsidy discipline with broadband-led acquisition

Spectrum’s wireless strategy is fundamentally a fixed-mobile bundling strategy; wireless is the retention and monetisation layer for its broadband footprint. Spectrum’s smaller promo volume and heavy trade-in dependency indicate strict control of subsidy exposure. Its best handset value is tied to new broadband + multiple lines, ensuring promotions are paid back through household economics rather than wireless-only profitability.

Xfinity Mobile: service-credit disruptor that converts broadband homes into mobile lines

Xfinity’s model is a convergence flywheel: subsidise service to win lines, then upsell plan tiers and devices selectively. Xfinity uses a powerful 12-month service credit to make entry-level unlimited effectively free (with qualifying internet). Device discounts then steer customers toward Xfinity Premium Unlimited + trade-in, blending acquisition with ARPU uplift.

Verdict

The handset market is being used as the subsidy wrapper around the real price – services revenue. Promotions increasingly function as plan-tier escalators (premium unlimited), convergence hooks (mobile + broadband), and multi-line builders (household economics), with free phone headlines often masking strict eligibility and long credit tails that harden retention.

The next phase of competition will be defined less by who offers the biggest discount and more by who can target it most efficiently while expanding service revenue by account.