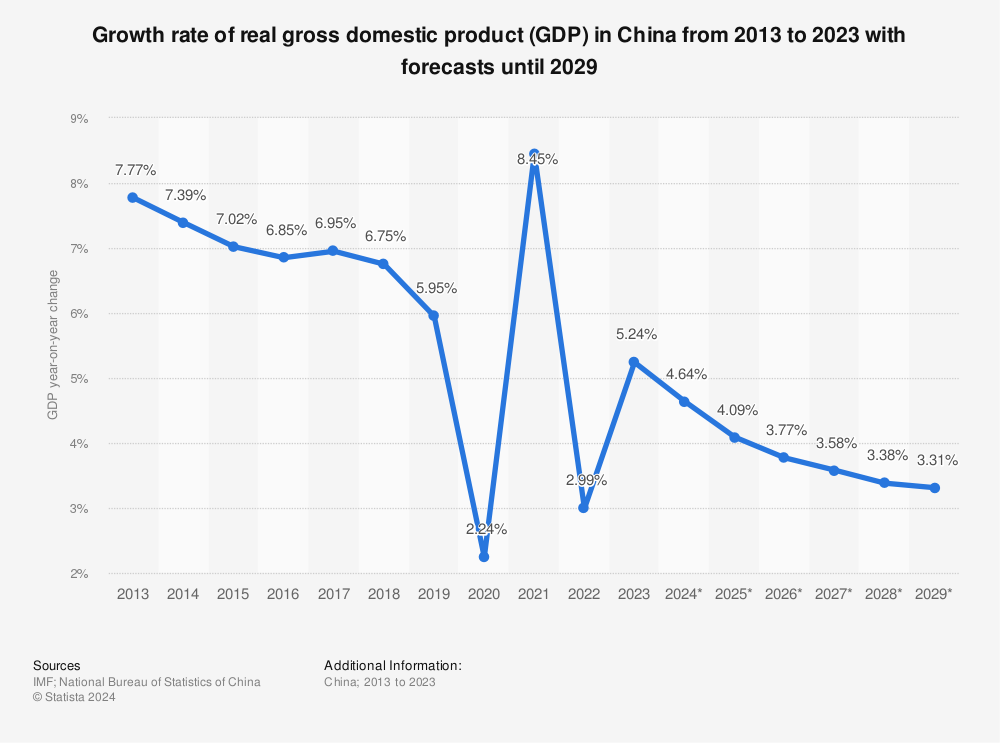

China’s economy grew 6.8% in the first quarter, above the government’s target of 6.5%, defying warnings that the country’s growth could slow in 2018.

Robust consumer spending, underpinned by stronger than expected global growth, gives Chinese authorities room to drive down borrowing. China has been fighting to contain ballooning debt and a housing bubble without hurting growth over recent years.

Go deeper with GlobalData

Access deeper industry intelligence

Experience unmatched clarity with a single platform that combines unique data, AI, and human expertise.

Meanwhile, the industrial sector showed signs of a modest slowdown.

An unexpected strong trade surplus boosted growth in 2017. The first quarter of 2018’s growth rate is compared with the same period last year.

The latest GDP figures are also above Beijing’s 2018 annual growth target of ‘around 6.5%’. However, forecasters generally still expect Chinese growth to cool for the year.

China’s President Xi Jinping said at a news conference:

China is fully capable of responding to Sino-US trade frictions, responding to challenges and maintaining sustained and healthy economic development.

There is however — as always with official economic data coming out of China — suspicions over its accuracy.

Erik Britton of Fathom Financial Consulting told BBC’s Radio 4 Today Programme his independent research suggests China’s economy is though growing at around 6.8%.

In our estimation there are 4.4 billion square metres of unused, unsold residential property stock that’s under construction right now – that’s enough to house 150 million people, which is large even by Chinese standards.

All of this is indicating a huge, colossal build up of excess capacity.

The analyst reaction

Cui Li, head of macro research at CCB International Holdings in Hong Kong, told Bloomberg Television:

The picture is pretty robust … Consumption is very strong, so that’s in line with the rebalancing story.

Bloomberg‘s own economists Tom Orlik and Fielding Chen said:

The steady expansion in GDP shows the economy shaking off threats from deleveraging and protectionism. Even so, a lower reading for nominal growth is a warning sign that the industrial reflation cycle that drove profits higher and made debt repayment more manageable in 2017 is turning down.

Iris Pang, greater China economist at ING, said:

China’s GDP grew strongly in 1Q18. But we underestimated the spending power of consumers and overestimated the role of fixed asset investments. The future for GDP rests on the uncertainty of trade and related industries.

Trade is far more than the net sum of exports and imports. It affects production chains, employment, investment and prices and therefore profit margins.

If trade tensions between China and US escalate, both economies will face tougher business environments. It will be a lose-lose result for any parties involved in a material trade war.

Rob Subbaraman, chief economist for Asia ex-Japan at Nomura Holdings in Singapore, said:

March data point to nascent signs of a growth slowdown underway, led by old economy sectors. We don’t expect growth in new economy sectors to fully offset the slowdown in the old, heavily-indebted sectors of the economy in the quarters ahead. This is a necessary adjustment to improve the quality of China’s growth.

Nomura analysts said:

March activity data largely slowed after a strong performance in January-February, which we judge was partly driven by the relaxation of strict pollution curbs. Industrial production growth eased to a weaker-than-expected 6.0% y-o-y from 7.2% in January-February … led by utilities and mining sectors.

The rebound in property investment growth continued, to 10.4% y-o-y ytd in March, while growth of property newly started and land sales also rose. That said, property sales growth, a leading indicator of property investment, continued to drop to 3.6% y-o-y ytd, pointing to downward pressures on the property sector.

Looking ahead, weaker March activity data support our view that there will be an economic slowdown ahead, driven by cooling investment growth, financing deleveraging, structural reforms which bring short-term pain, and rising trade protectionism.

Betty Wang and David Qu, China economists at ANZ, said:

We do not think the slowdown in nominal GDP growth and its implied GDP deflator indicates any deterioration in China’s debt mechanism.

But China’s latest efforts in cracking down on the shadow banking sector and directing credit back to the real economy will likely help alleviate its debt pressure and mitigate risks.

More importantly, relying less on leverage to boost GDP growth via structural reforms instead of depending on inflation to gradually dilute the debt-to-GDP ratio is the key to resolve China’s debt issue, from a longer term perspective.

Louis Kuijs of Oxford Economics said:

China’s economy entered 2018 with solid growth momentum. But momentum slowed in March, compared to the first two months, pointing to slower growth ahead.

Yue Su, China economist at the Economist Intelligence Unit, said:

The acceleration in property development investment reflects a funnelling of household funds into the sector.

However, with the central government still tightening real estate companies’ access to credit and focused on controlling household leverage ratios, the sector will likely cool later in the year. The central government is also tightening the approval of infrastructure projects due to local government debt concerns.

Challenges for the remainder of the year include managing probably excessively strong investment growth in the services sector while encouraging a revival in weak industrial and manufacturing investment.

Julian Evans-Pritchard, senior China economist at Capital Economics, said:

While we don’t think China’s economy is expanding as rapidly as the official figures claim, there is broader evidence to suggest that a recovery in industry did prevent growth from slipping too much last quarter.

But outside of industry, activity looks to have cooled recently.

Looking ahead, while the Chinese economy held up fairly well in Q1 we think a further slowdown is on the cards before the end of the year. In particular, the one-off boost to industrial production from the easing of pollution controls should fade before long and the drags from tighter fiscal policy and slower credit creation will continue to weigh on broader activity.