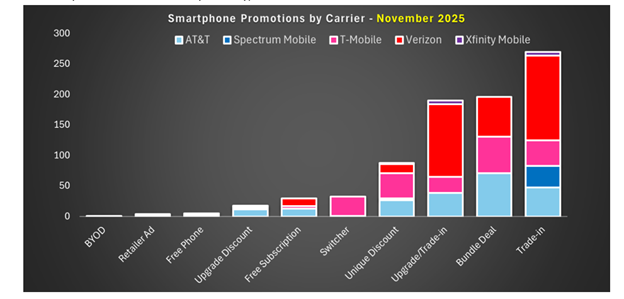

In November 2025, a total of 835 promotions were launched, spanning ten distinct promotional formats across Verizon, AT&T, T-Mobile, Spectrum Mobile, and Xfinity Mobile.

Verizon led all carriers in promotional volume, followed by AT&T and T-Mobile, while Spectrum Mobile and Xfinity Mobile continued to refine their MVNO-driven value strategies.

Go deeper with GlobalData

Access deeper industry intelligence

Experience unmatched clarity with a single platform that combines unique data, AI, and human expertise.

Device prioritisation skewed heavily toward premium OEMs: Samsung accounted for some 521 promotional listings, while Apple saw approximately 207, underscoring the industry’s continued reliance on high-end flagships to steer service tier upgrades and long-term account value.

Black Friday activity proved relatively muted. Verizon and T-Mobile focused on standard ecosystem-based bundle offers around Samsung, Apple, and Google products, while Xfinity Mobile offered predictable trade-in and new line deals centered on major OEMs. Rather than dramatic holiday undercutting, carriers maintained strategic restraint, signaling confidence in year-round promotional architectures rather than single-week blowouts.

Strategic promotional posture

- Verizon pursued maximum ARPU expansion and multi-device locking. Its promotions paired substantial device discounts with value-added service bundles to anchor customers in premium, high-yield plans.

- AT&T leaned into consistency, fairness, and broad eligibility, positioning transparent, accessible offers as a differentiator.

- T-Mobile balanced aggressive device incentives with a deliberate push toward Experience Beyond and Experience More premium tiers.

- Spectrum Mobile and Xfinity Mobile used trade-in offers and tiered premium plans to push customers toward device purchases and higher-value service plans. Their strict plan rules serve dual purposes: rewarding loyal customers while safeguarding against margin compression.

Across all carriers, trade-in promotions remain the linchpin for easing consumer cost burdens and stimulating cyclical device upgrades. Bundle ecosystems featuring service and devices are increasingly used as value differentiators rather than simple incentives.

A key structural theme is the prominence of plan-tier gating. Verizon’s Unlimited Plus, T-Mobile’s Experience Beyond/More, and Xfinity’s Premium Unlimited all demonstrate a coordinated industry pivot toward ARPU-focused tier migration. These constraints funnel customers into higher-value service stacks while keeping promotional costs controlled.

At the same time, transparency is rising as a competitive asset. AT&T’s open eligibility and Spectrum Mobile’s simplified trade-in terms reflect a growing recognition: customers are increasingly fatigued by restrictions, hidden requirements, and complex upgrade conditions.

Promotions verdict

The November 2025 promotional landscape makes one fact clear: carriers are no longer selling discounted devices—they are engineering ecosystems designed to lock in retention, elevate ARPU, and minimise churn. The device deal is merely the entry point. For consumers, the environment offers richer trade-in values and more meaningful bundles, but navigating eligibility, plan tiers, and upgrade constraints remains a significant challenge.

Ultimately, carriers that will win in the next competitive cycle are those able to pair bold incentives with transparent terms, frictionless switching, and value-anchored service bundles that reinforce long-term loyalty