February 2026 confirms that the US smartphone market has settled into a high-volume, highly repeatable promotional equilibrium where the “deal” is no longer a seasonal tactic but a core sales system.

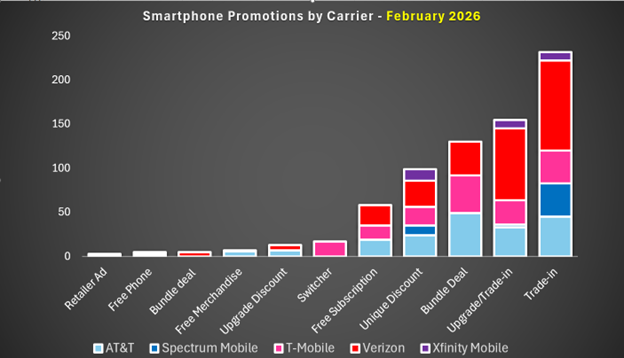

Across AT&T, T‑Mobile, Verizon, Spectrum Mobile, and Xfinity Mobile, GlobalData tracked 724 new smartphone promotions across 11 distinct promotion types, with trade-in (for both upgrades and new lines) and bundle offers dominating the mix. Verizon (289 offers), AT&T (186), and T‑Mobile (164) collectively set the pace, while Samsung and Apple absorbed the bulk of subsidy attention, accounting for roughly 473 and 199 offers, respectively.

Go deeper with GlobalData

Access deeper industry intelligence

Experience unmatched clarity with a single platform that combines unique data, AI, and human expertise.

Carriers promote premium plan adoption and bundles

Verizon’s approach was the clearest expression of “premium-plan monetisation via flagship demand.” Its promotions scale sharply by unlimited tier, with the richest credits reserved for Verizon Unlimited Ultimate, followed by Unlimited Plus, while Unlimited Welcome remains a lower-incentive entry ramp. The Samsung Galaxy S26 series launch was the anchor: the Samsung S26 Ultra reached up to $1,300 for eligible trade-in upgrades on Ultimate, while new-line credits remained substantial across tiers. This structure is effective at driving ARPU and reducing churn by rewarding upgrades, but it also increases consumer decision complexity and pushes value-sensitive customers toward either new-line options or lower tiers with materially weaker savings. Verizon is winning on volume and device visibility, but risks perception of “strings-attached” value if the offer ladder becomes too opaque.

AT&T’s promotional stance was more measured and operationalised—less about flash and more about consistency. With emphasis on bundle deals, trade-in, and upgrade-with-trade-in mechanics, AT&T signalled a “steady-state” model intended to support retention and predictable gross adds. Its Samsung Galaxy S26 offers (up to $1,300 / $1,100 / $900 with trade-in on AT&T Unlimited Starter SL) were competitive, and the tiered trade-in thresholds showed disciplined subsidy control. The companion-device bundle (Tab / Watch at $0.99/month on Value Plus) reinforced AT&T’s ecosystem strategy to create incremental attachment value. The risk is that “always competitive” can feel indistinct; AT&T must ensure its simplicity message cuts through when rivals are shouting “free.”

T‑Mobile continued to weaponise promotional frequency and segmentation. The carrier combined bundles and trade-ins with aggressive conversion tactics, notably using Metro as a funnel into postpaid via high-dollar device credits on the T-Mobile Essentials plan. Its Samsung Galaxy S26 strategy mirrors Verizon’s upsell ladder—highest value on premium T-Mobile Experience tiers—while adding differentiation through network-level features such as “Live Translation”. If executed well (latency, accuracy, privacy), this is strategically meaningful: It’s a service-native benefit that could reduce reliance on escalating subsidies. The risk is execution and trust; without clear safeguards, AI-in-the-network could become a hesitation point rather than a hook.

Cable MVNOs court convergence

Cable MVNOs are converging toward parity pricing and convergence-led acquisition. Spectrum’s sharp shift—80% of promos requiring trade-in alongside a $10 single-line price increase—signalled a deliberate move to protect service ARPU while funding device discounts through customer equity (their old phones). Xfinity, meanwhile, leaned hardest into “free mobile with broadband,” using a $40/month credit to effectively zero out base unlimited for a year, then upselling Xfinity Premium Unlimited with stronger device incentives and fee waivers. The verdict for cable: convergence is now table stakes, not differentiation; the winners will be those who best manage subsidy costs while converting promotional trial into long-term, multi-product households.

The verdict

The market is being shaped less by occasional blockbuster discounts and more by plan-gated, trade-in-funded subsidies designed to steer behaviour—upgrade timing, plan tier selection, and multi-line expansion.

Overall, February’s landscape showed a market optimised for controlled subsidy economics: trade-ins as the funding mechanism, plan tiers as the steering wheel, and Samsung / Apple launches as the recurring ignition. The next competitive frontier is not bigger discounts, but clearer value, fewer conditions, and durable service-led differentiation that outlasts the bill-credit term.