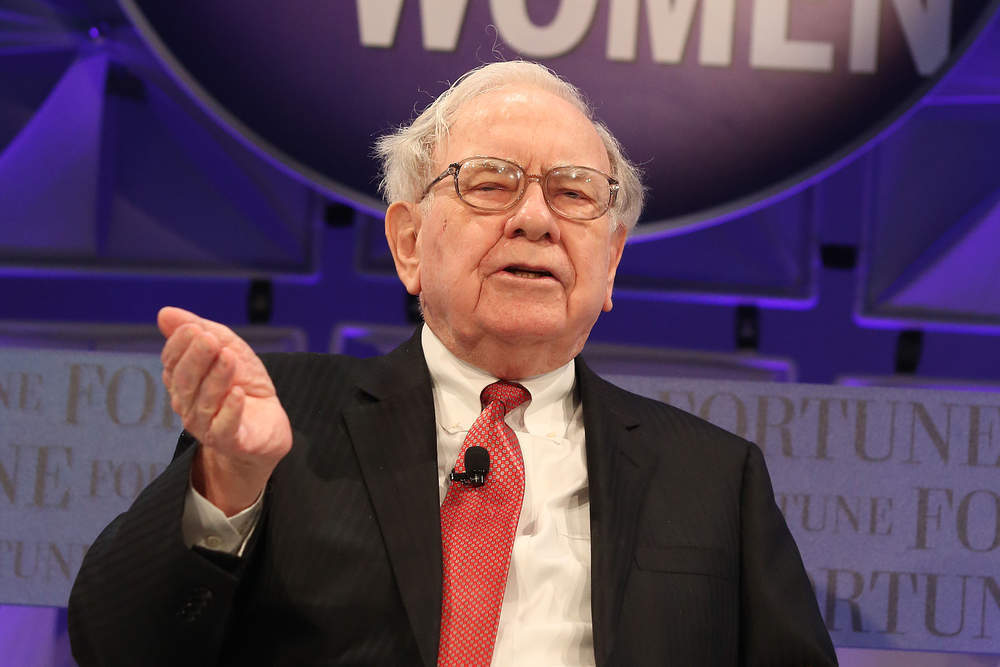

There are few individual people the market listens to as closely as it does to Warren Buffett. When the Oracle speaks, investors pay attention.

Buffett — the CEO of investment giant Berkshire Hathaway — owns stocks in a wide range of US companies and financial institutions, including GEICO, Wells Fargo, American Express, Coca-Cola, Goldman Sachs, and American Airlines.

Go deeper with GlobalData

Access deeper industry intelligence

Experience unmatched clarity with a single platform that combines unique data, AI, and human expertise.

Buffett is known as the Oracle of Ohama for his impressive track record of stocks picks and his market commentary.

Over the weekend he released his letter to shareholders and yesterday participated in his customary annual interview with CNBC.

These included Buffett sharing his expert insights on sensible financial investing practice and the state of the American economy.

The top five things we learnt from Buffett this week

1. Long-term investors should buy stocks over bonds

Buffett refuses to subscribe to the belief within some parts of the financial system that bonds are a lower-risk investment over the long term. He recommends that investors stay in equities because inflation and purchasing power has a greater effect on bonds than stocks.

Buffett told CNBC:

“If you had to choose between buying long-term bonds or equities, I would choose equities in a minute.

“If I were going to own a 30-year government bond or own equities for 30 years, I think equities will considerably outperform that 30-year bond.”

In his investor letter, Buffett wrote:

“I want to quickly acknowledge that in any upcoming day, week or even year, stocks will be riskier — far riskier — than short-term U.S. bonds.As an investor’s investment horizon lengthens, however, a diversified portfolio of US equities becomes progressively less risky than bonds, assuming that the stocks are purchased at a sensible multiple of earnings relative to then-prevailing interest rates.

“He said that investors would be much better off if “they just think of stocks as pieces of business .. rather than thinking of them as little things that move around in price.”

2. Business leaders must be careful about imposing their personal views on their organisations

In the context of certain US companies cutting their partnerships with the US National Rifle Association following the Parkland high school massacre in Florida this month, Buffett commented that he did not think that business leaders should impose their personal views on their clients or their employees.

He told CNBC:

“I don’t believe in imposing my views on 370,000 employees and a million shareholders. I’m not their nanny on that.

“You have to be pretty careful if you’re saying that you’re not going to fly on this airline because of that or we’re not going to use this railroad because of that.

“I don’t think that Berkshire should say we’re not going to do business with people who own guns. I think that would be ridiculous.”

3. Investors should avoid using borrowed money to make investments

Buffett described borrowing money on securities as “madness”.

“Berkshire, itself, provides some vivid examples of how price randomness in the short term can obscure long-term growth in value. For the last 53 years, the company has built value by reinvesting its earnings and letting compound interest work its magic.

“Year by year, we have moved forward. Yet Berkshire shares have suffered four truly major dips.

“You do not know whether the stock exchange will open tomorrow morning… It is insane to risk what you have and need for something that you don’t really need.”

This opinion is consistent with Buffett’s aversion to unnecessary risk. He wrote in his investor letter:

“Our aversion to leverage has dampened our returns over the years… [We] believe it is insane to risk what you have and need in order to obtain what you don’t need.

“We held this view 50 years ago when we each ran an investment partnership, funded by a few friends and relatives who trusted us. We also hold it today after a million or so ‘partners’ have joined us at Berkshire.”

4. Apple continues to be an attractive investment

Buffett declined to answer which of his holdings he would theoretically invest all of his stocks in. However, he did note that what he had bought recently was an indicator of what he would perceive to be a good investment.

“If you look… in terms of recent purchases over the last year we’ve bought more Apple than anything else.”

According to its investor letter, Apple is now Berkshire Hathaway’s second biggest holding. Its market value position equals $28.2 billion.

In Buffett’s view the technology giant remains an attractive.

“Apple has an extraordinary consumer franchise.”

“I see how strong that ecosystem is, to an extraordinary degree … You are very very very locked in at least psychologically and mentally to the product you are using. [IPhone] is a very sticky product.”

He admits that although he does not own a smartphone, which he says is a sign that the market is not yet saturated, if he were to buy one it would “definitely” be an Apple product.

5. Lowering of corporate tax rate in the US is a “huge tailwind” for domestic businesses

Despite not supporting the reduction of federal corporate tax implemented in December which reduced the rate from 35% to 21%, Buffett recognised that this would provide a “huge tailwind” for US businesses.

He believes that the savings from these tax changes will stimulate the US economy for years to come because companies will reinvest in their businesses and keep their operations on home soil.

Buffett believed that the old corporate tax rate was not hurting US businesses in the world economy.

He told CNBC:

“When we make money in 2018 domestically, and subject to a lot of little things here and there, basically we’ll be paying at 21 percent instead of 35 percent. That’s a lot of money.

“It’s particularly a tailwind if you’ve got … lots of deprecation and taken bonus deprecation upfront. So it’s a big item there.”

Berkshire Hathaway recorded a $65 billion increase in net worth in 2017 — $29 billion was due to the tax reform. This gain from the tax changes exceeds four of the last five total gains for the conglomerate.