April 2026 confirms a US smartphone market operating in a promotion-first equilibrium, where scale, structure, and plan design—not just discount depth—determine competitive outcomes. Activity was led by Verizon (424 offers), followed by T‑Mobile (231) and AT&T (185), while cable MVNOs executed smaller but highly targeted playbooks. The device mix remained concentrated around flagships, with Samsung (576 offers) and Apple (261) dominating, underscoring the continued importance of premium devices to drive both acquisition and upgrade cycles.

Verizon verdict: promotion-led growth, disciplined by plan laddering

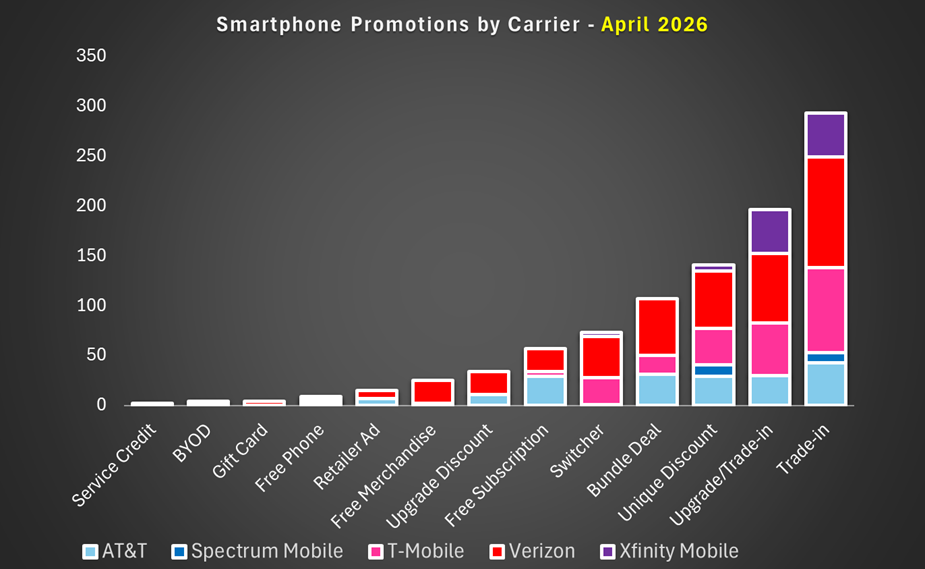

Verizon is running the most overtly promotion-led strategy, using handset incentives as an ARPU and retention engine. April’s mix leaned heavily into trade-ins (111) and upgrade/trade-in variants (69), supported by meaningful bundle activity (57). The defining feature is strict plan laddering: The richest device credits are gated behind Unlimited Ultimate, then Unlimited Plus, while Unlimited Welcome receives reduced promotional support.

Verizon also tightened BYOD economics at the low end by cutting the Welcome BYOD reward to $180 over 36 months. Monthly crediting, compatible-device requirements, and one-line-per-account limits reduce leakage and improve payback certainty. Results indicate momentum: 55,000 Q1 2026 postpaid phone net adds (first positive Q1 since 2013), 0.97% churn, and a 3% upgrade rate.

AT&T verdict: repeatable value propositions and convergence-led retention

AT&T is shifting away from headline-grabbing, one-off deals toward repeatable, scalable promotions that shape predictable customer behaviours. Its 185 April promotions were concentrated in trade-ins (43) and bundles (31), signalling preference for controllable levers like upgrade cadence and multi-product attachment. The launch of Elite 2.0 ($110 with autopay) reinforces a value-packaging strategy to increase switching costs and deepen ecosystem lock-in.

AT&T also adjusted its family plan architecture by lowering Unlimited Premium 2.0 to $50/line for four-plus lines, narrowing the gap with competitors, though T‑Mobile’s “third line free” still wins on new-customer price math. Q1 supports the direction: 294,000 postpaid phone net adds, 0.89% churn, and a 3.5% upgrade rate, with convergence (wireless + home internet) central to growth quality.

T‑Mobile verdict: always-on execution with monetisation discipline

T‑Mobile remains the archetype of high-frequency, always-on promotions, using constant refreshes to sustain retail traffic and switcher velocity. April’s 231 new offers leaned into trade-ins (85) and new line promos (36), typically structured to push premium tiers and multi-line households—key drivers of lifetime value.

Its $200 BYOD offer functions as a targeted acquisition tool: Port-in and rebate compliance requirements control subsidy exposure, while faster perceived value improves conversion versus long-duration bill credits. Q1 performance indicates growth without major retention tradeoffs: 217,000 postpaid net account adds, 1.04% churn, 2.8% upgrade rate, and ARPA up 3.9% YoY to $151.93, supported by network leadership as a differentiator.

Cable MVNO verdict (Spectrum + Xfinity): convergence wins, but margins must be managed

Spectrum Mobile is pursuing margin-aware growth: only 22 handset promotions, with ~46% requiring trade-ins, using recovered value to limit subsidy spend. Charter posted 344K Q1 residential line adds, 11.7M total lines (+16.8% YoY), and $1.05bn mobile service revenue (+15.1% YoY).

Xfinity Mobile is scaling convergence aggressively: 435,000 Q1 line adds to 9.7 million lines (~16% broadband penetration). Wireless service revenue rose 15% to $977m, while equipment revenue surged 53% to $418m, consistent with heavier device promotions and upgrades. New Mobile Select ($30) and Mobile Plus ($45) tiers sharpen segmentation, while its “free year of mobile” promo positioning targets broadband households with controlled subsidisation and upsell paths.

Verdict: intensity isn’t falling—it’s becoming more efficient

The market is not reducing promotional intensity; it is professionalising it. Winning strategies combine always-on trade-ins, plan gating, bundled value, and tight eligibility controls to protect unit economics. Cable MVNOs demonstrate that targeted convergence can scale wireless growth without matching national-carrier promo volume—so long as subsidy exposure is actively managed.