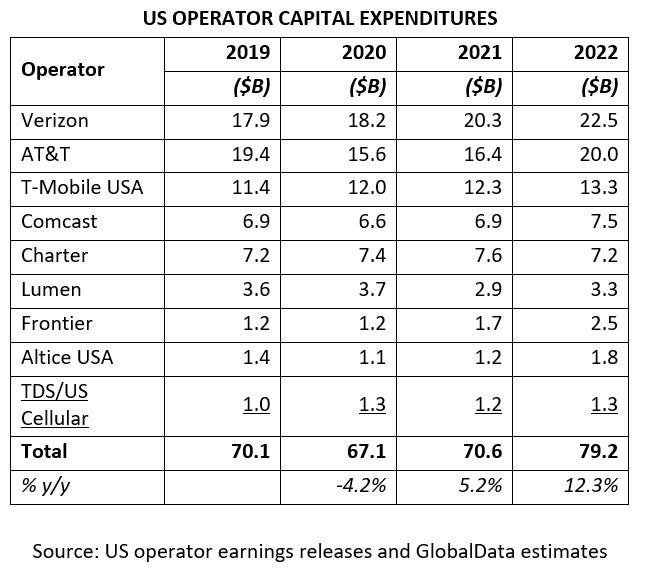

An analysis of US operator financial results based on Q4 2021 earnings releases shows that CapEx in 2021 came in nearly identically to 2019 levels after a Covid-driven dip in 2020. The nine network operators shown below – all of which spent more than $1 billion in CapEx – spent $70.6 billion in 2021 CapEx, up 5.2% from 2020 and nearly flat from 2019. GlobalData estimates that the big three that account for nearly 70% of total CapEx – AT&T, Verizon, and T-Mobile USA – spent roughly $49 billion, up 7% from 2020.

That spending is poised to jump in 2022, based on guidance provided alongside year-end 2021 results. GlobalData estimates that next year’s spend among these US operators will be up by $8.6 billion, a double-digit percentage increase, to $79.2 billion.

There are two primary factors accounting for the increased spending planned in 2022. For Verizon and AT&T, aggressive plans to deploy 5G in midband spectrum are fuelling significant deployment activity. In addition, a host of operators – including AT&T, Altice USA, and Frontier – are planning to deploy fiber more extensively across their networks.

A scan of international operator results shows a similar trend of post-pandemic CapEx increases in 2021; however, major multinational operators in Europe have taken more of a ‘steady as she goes’ approach to 2022 guidance. For example:

- Telefónica significantly increased its CapEx from €5.9 billion to €7.3 billion in 2021, and it appears poised to maintain 2021 spending levels in 2022.

- Orange’s CapEx increased from 2020 to 2021, from €7.1 billion to €7.7 billion. However, Orange expects CapEx to decline slightly, to less than €7.4 billion in 2022.

- Deutsche Telekom CapEx spending was flat in 2020 and 2021 at €7.7 billion (excluding investments toward T-Mobile USA). DT expects a slight increase in 2022 driven mainly by spending in its domestic German market.

One more positive note from year-end results: few operators have expressed specific concerns over supply chain constraints that could potentially slow their deployment activity. As a result, 2022 is shaping up to be a very busy year for network infrastructure vendors.