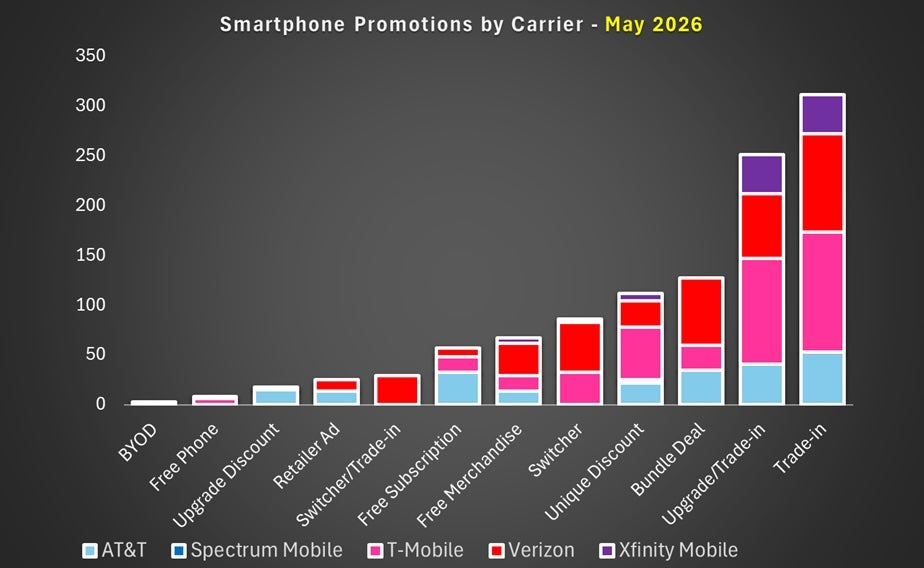

May 2026’s US smartphone promotional landscape reflects a mature, high-frequency subsidy market where carriers are using device offers less as blunt acquisition tools and more as precision instruments to steer customers into higher-value plans, longer commitments, and multi-product ecosystems. With 1,094 new deals across five major operators and 12 distinct promotion types, the month confirms that promotions are now “always on,” operationalised similarly to a pricing layer. The volume concentration—Verizon (394), T-Mobile (376), and AT&T (227)—also shows that the national carriers continue to set the competitive tempo, while cable MVNOs participate selectively and tactically.

The device mix underscores where competitive energy sits. Samsung (600) and Apple (310) dominate promotional attention because they anchor premium plan attachment and generate predictable upgrade cycles. In practice, their flagships and foldables function as carriers’ most effective levers for ARPU expansion: rich bill credits are routinely gated behind premium unlimited tiers. The result is a market where “free” or “$0/mo.” phones are rarely free—rather, they are financed through plan upsell, tenure, and account expansion.

Go deeper with GlobalData

Access deeper industry intelligence

Experience unmatched clarity with a single platform that combines unique data, AI, and human expertise.

Verizon’s approach is the clearest example of monetisation-first promotions. Its trade-in heavy playbook and bundling with tablets/wearables is designed to reduce churn and widen share-of-wallet, not merely win switchers. Even when Verizon sweetens deals — such as making the Motorola Razr 2026 effectively free via an $800 trade-in credit — it pairs the offer with plan requirements and broader ecosystem hooks. Verizon’s simultaneous price/perk adjustments (e.g., raising Verizon Unlimited Ultimate while adding premium features) reveal a carrier confident enough to test price elasticity while using promotions to keep perceived value high.

AT&T, by contrast, is standardising promotions into repeatable, value-driven mechanics—trade-ins, bundles, and long-duration bill credits—favouring predictability over flash. Its veteran-targeted credits and 36‑month instalment structures emphasise retention through commitment. AT&T’s “Build‑A‑Plan” is a smart counterbalance: it attracts price-sensitive BYOD users without heavy subsidies, offering a controlled way to add subscribers while limiting promotional exposure.

T-Mobile remains the most aggressive and segmented operator, running a true continuous-promo engine. Its differentiated incentive tiers—premium Apple iPhone offers tied to top T-Mobile Experience plans, elevated Samsung credits to win value-tier switchers, and frictionless Motorola deals without trade-ins—signal a carrier optimising for multiple funnels at once. The common thread is plan gating: Even when trade-in friction is removed, profitability is defended through premium plan attachment.

Cable MVNOs show diverging strategies. Spectrum Mobile’s minimal activity suggests a conservative posture, using modest discounts mainly to add lines. Xfinity Mobile, however, is behaving more like a scaled promotional competitor: heavy trade-in dependence to fund rich credits and a notable enhancement to Xfinity Mobile Plus (up to six upgrades/year) that targets high-churn, tech-forward customers with retention-friendly flexibility. Overall, the market is not discounting more—it is discounting smarter. Promotions increasingly exchange device value for higher recurring service value, deeper ecosystem entanglement, and longer customer lifetimes. Winners will be those who pair clear, simple offer design with targeted subsidy investment and plan innovation; losers will be those whose promotions add complexity without creating durable ARPU lift or churn reduction.